With a Brexit trade deal agreed and an aggressive vaccine programme in place, Trustnet asks several fund managers whether 2021 will be a turnaround year for the UK market?

The UK has consistently been out of favour with investors for several years since the referendum on EU membership in 2016, which brought great uncertainty to the UK market and kept many overseas investors away.

This was compounded by the impact of the Covid-19 pandemic last year, which initially saw a flat-footed response to tackling the coronavirus.

The economic response to the virus favoured growth style companies – supported by all-time low interest rates, ultra-loose monetary policy and fiscal measures.

However, the UK is predominantly a value market, with the market dominated by oil, banks and financials which all took major hits and struggled to recover.

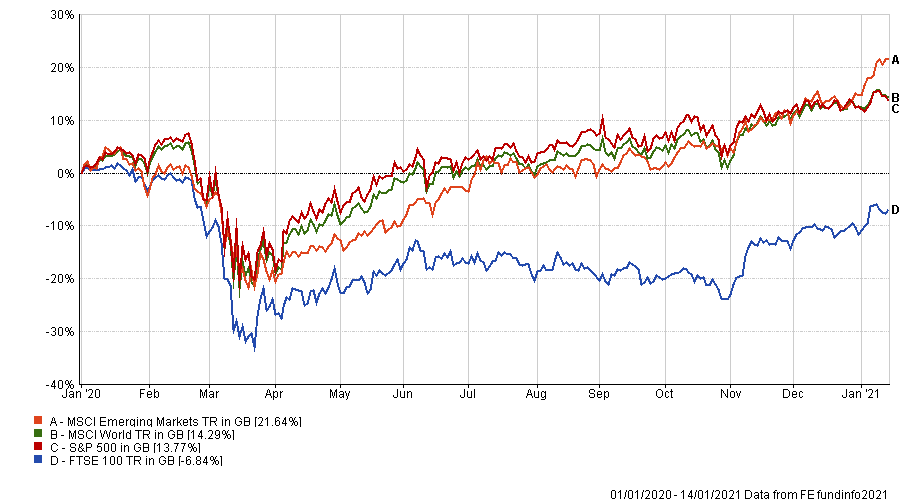

Performance of major indices in from 1/1/2020 to date

Source: FE fundinfo

But now the UK has secured a post-Brexit trade deal and – despite a third national lockdown – implemented an aggressive vaccine programme, will 2021 be a more positive year for the UK?

One thing the managers Trustnet spoke with think, is that the UK market will see the return of overseas investors.

Manager James Thomson (pictured), who runs the Rathbone Global Opportunities Fund, said that the Brexit trade deal has made the UK an option for overseas investors again.

He said: “Brexit clarity has put the UK back on the menu for international investors. Never underestimate the grit, adaptability and foresight of British business.”

Like many overseas investors Thomson had stayed away from UK equities due to the uncertainty. But with that now gone the FE fundinfo Alpha Manager said he has increased his UK weighting for the first time in four years, indicating a more positive outlook on the UK going forward.

“However, we’re not getting too carried away,” he said. “So, while our UK weighting may increase over the coming months, we don’t expect a dramatic return to pre-Brexit weighting [25 per cent] – that’s way off – as we still have a long list of US and European ideas.”

Ken Wotton, who runs the Strategic Equity Capital fund, added that for UK small caps especially the trade deal could acts as “a catalyst to revive investor interest in the UK”.

Wotton said with UK companies now able to plan ahead more clearly, combined with a return of overseas investors, we should start to see the discounts on UK assets narrowing.

He said: “And so all else being equal – which is a pretty big caveat given Covid – those discounts, both the UK versus other markets, and also UK small-cap versus the rest of the UK market should start to narrow.

“And that’s certainly how we’re anticipating this year to pan out.

“It’s very anecdotal, but I’m certainly getting the sense that some asset allocators are starting to look again at the UK as sort of good value. And although it’s hard to be definitive if we do start to see material inflows that that should help those discounts to narrow.”

Richard Colwell, fund manager and head of UK equities at Columbia Threadneedle, also believed the UK discount could start to narrow.

According to the manager, the opportunity in the UK was shown by the market’s reaction to the Pfizer and BioNTech vaccine in November, which saw months of growth stocks outperformance undone as value names surged.

“We continue to firmly believe in the UK, but trends often go on for longer than predicted,” he said. “This creates the opportunity we see today, as it amplifies the impact when the switch in momentum finally occurs.

“However, the window on unlocking this potential value is closing. While sentiment about the UK economy has been hurt by both Covid-19 and Brexit, the equity market does not need a great recovery to perform better.”

Forecasting a “reasonable recovery in 2021”, Columbia Threadneedle’s Colwell (pictured) said there was a limited window to take advantage of the UK opportunity.

He said: “As the UK’s double discount starts to narrow, following the greater clarity that Brexit should bring and as vaccines progress, 2021 and into 2022 could be exciting for the UK equity market.

“Even the UK’s quality growth companies like Unilever are a lot cheaper than their rivals globally. We believe it’s not just one or two areas of the UK market that are cheap; the whole market is cheap.”

Taking advantage of these current discounts in the UK, Nick Kirrage – co-head of the Schroder Global Value team – said the value-oriented portfolio will be looking for those opportunities in 2021.

He said: “Despite a strong rebound in the autumn, the UK remains one of the cheapest developed stock markets globally. We see real opportunities in the banks, energy and food retail where we feel valuations are too cynical and dismiss economic reality.

“While the vaccine programme and a conclusion to the Brexit negotiations remove some of the uncertainty investors have been grappling with when looking at the investment case for UK plc, we believe the biggest returns will come from those unloved companies that many are dismissing.

“We will continue trying to capitalise despite the bad headlines, using our disciplined valuation-based approach.”

But while Brexit has been a major issue for UK equities the biggest challenge will be the ongoing pandemic, according to Gresham House’s Wotton.

He said: “To be honest, Covid has been a much bigger test of this than Brexit. As [with] Brexit you’ve had time to get used to the idea to think through the risks and the opportunities and to plan for it. Covid was much more stark and much more rapid.

“I think it’s been a real test of managements. And actually, it’s been a sort of diligence to assess the quality management over the past 12 months.”

Going forward he said that he’s more focused on his fund’s positioning around Covid and the impact it’s had, which he thinks is more significant for the UK market.